Dominic Volek, CA(SA), FIMC, is Group Head of Private Clients and a Member of the Executive Committee at Henley & Partners.

Global risk is being rapidly repriced — and investors are already responding.

The 2026 special edition of the Global Investment Risk and Resilience Index (GIRRI) shows a clear re-ranking of countries, with positions shifting materially over a short period of time. What is equally striking is how closely investor behavior is tracking that shift. Families are not waiting for stability to return. They are acting on changing conditions in real time, adjusting both capital allocation and personal exposure across jurisdictions.

This is not a temporary response to a single shock. It reflects a deeper structural change in how internationally mobile investors approach residence and citizenship planning.

For much of the investment migration industry’s history, residence and citizenship by investment programs were treated as contingency planning — a form of insurance acquired in response to a specific risk and often left unused. That model is no longer sufficient.

What we are seeing now is a shift towards permanence. Residence and citizenship rights are being integrated into the core architecture of wealth structuring, alongside trusts, holding companies, and asset allocation strategies. They are no longer simply a hedge against uncertainty. They are becoming a foundational component of long-term resilience.

The driver is not just rising volatility, but also the speed at which the global risk landscape is evolving. The updated Index makes this visible. Countries are moving relative to one another in ways that would have seemed improbable even a year ago. For investors, the implication is clear: no single jurisdiction, however strong, can provide sufficient protection against a world that is being repriced this quickly.

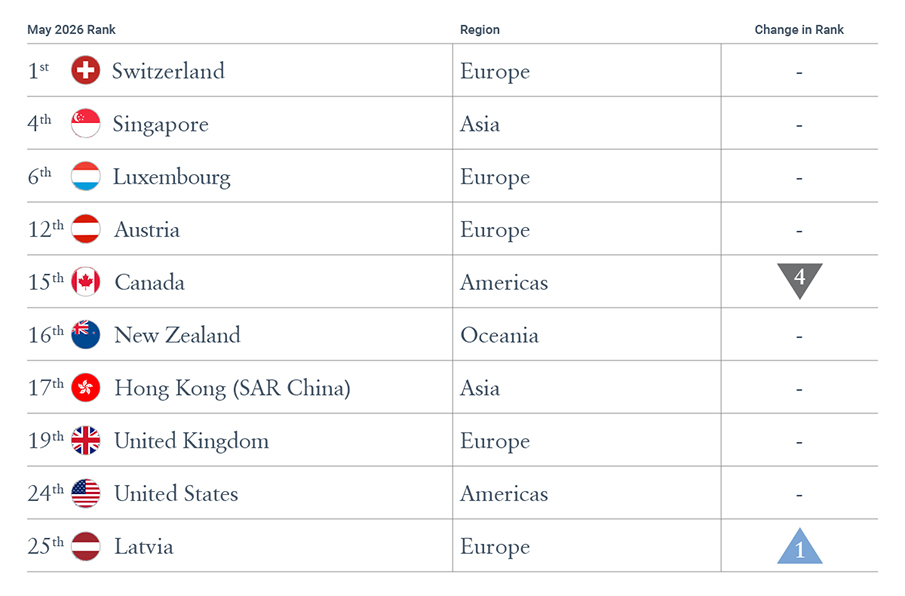

Table 1. Leading Countries with Residence and Citizenship Programs: GIRRI May 2026

Nine of the Top 10 countries offering residence or citizenship programs held their positions steady in the GIRRI May 2026 update, or recorded only marginal shifts. This stability underscores the ability of these jurisdictions to withstand extreme ‘stress test’ conditions, reinforcing their appeal for long-term residence and citizenship planning.

While Canada registered a moderate decline, this largely reflects stronger relative gains among other high-performing economies rather than a material deterioration in its own fundamentals.

The most important change in 2026 is not simply the volume of demand for alternative residence and additional citizenship, but its composition. Historically, the strongest growth came from families in jurisdictions experiencing visible instability or policy risk. That demand remains. But the more significant development is the rise in activity from investors based in some of the world’s most established economies.

We are seeing sustained growth across European markets, alongside increasing demand from North American and Asian clients. British and Canadian nationals continue to feature prominently among the most active globally, while US nationals represent the largest share of applications.

This is not a response necessarily to crisis conditions at home. It reflects a forward-looking assessment of a world in which relative positioning is shifting rapidly. The conclusion many of these investors are drawing is the same one captured by the Index: a single passport, however strong, is no longer sufficient. Sovereign optionality has moved from a secondary consideration to a primary one.

The practical response is the construction of multi-jurisdictional strategies. Rather than selecting a single destination, investors are assembling portfolios of residence and citizenship rights, each serving a distinct role within a broader structure.

The Gulf continues to function as a central operational and fiscal hub, with the UAE in particular acting as a platform from which many globally mobile families are building additional layers of diversification. At the same time, Southern European programs are attracting strong demand from those seeking long-term access to the European Union through clear and predictable frameworks, with Greece and Italy standing out in the current cycle.

Caribbean programs continue to serve families requiring speed and flexibility, particularly for mobility across the Western Hemisphere. Meanwhile, demand for geographically distant jurisdictions has increased sharply, reflecting a growing emphasis on physical separation from geopolitical risk combined with institutional stability. Interest in New Zealand, for example, has risen markedly as investors seek precisely this combination.

Across all of these markets, the pattern is consistent. Investors are no longer choosing between jurisdictions. They are combining them — building structures designed to function across a range of potential future scenarios.

The supply side is evolving just as quickly as demand.

On one side, governments are tightening frameworks — reconfiguring programs, increasing thresholds, and extending timelines, often in response to regulatory pressure or domestic political considerations. On the other, a growing number of jurisdictions are actively competing to attract mobile capital and talent, introducing new programs or refining existing ones to remain competitive in a more fluid global environment.

The result is not a simple contraction of supply, but a more dynamic and fragmented landscape. Availability, terms, and attractiveness can shift quickly, sometimes within a single policy cycle. For investors, this creates both opportunity and constraint. Favorable conditions are often transitional. Programs that are accessible today may be repriced, restricted, or withdrawn tomorrow.

In this environment, timing matters. The advantage increasingly lies with those who move early, while optionality is still available and before policy shifts narrow the field.

The implications for investors and advisors are straightforward. Residence and citizenship planning is no longer a discretionary add-on. It is becoming a core component of risk management and long-term continuity planning. The updated Global Investment Risk and Resilience Index provides the analytical framework for understanding how global risk is shifting. Investor behavior shows how that analysis is being translated into action.

Every decision to acquire an additional residence or citizenship reflects a recognition that reliance on a single jurisdiction is no longer sufficient — and is even naive. In a world where risk is being repriced and re-ranked in real time, mobility is not about convenience. It is about choice and control.

As the global leader in residence and citizenship planning, Henley & Partners is best placed to advise you and your family. Contact us for a free consultation.