Dr. Rahul Choudaha is Chief Operating Officer and Professor at the University of Aberdeen, Mumbai.

India’s rising wealth is driving a surge in demand for international education, making global mobility a central part of long-term family planning. According to Reserve Bank of India data, Indian families and students spent USD 3.71 billion in 2025 on international education — an increase of 31% compared to USD 2.83 billion in 2018. Yet new restrictions on student movement, alongside the rapid growth of international branch campuses (IBCs) in India, may well reshape how families access global education.

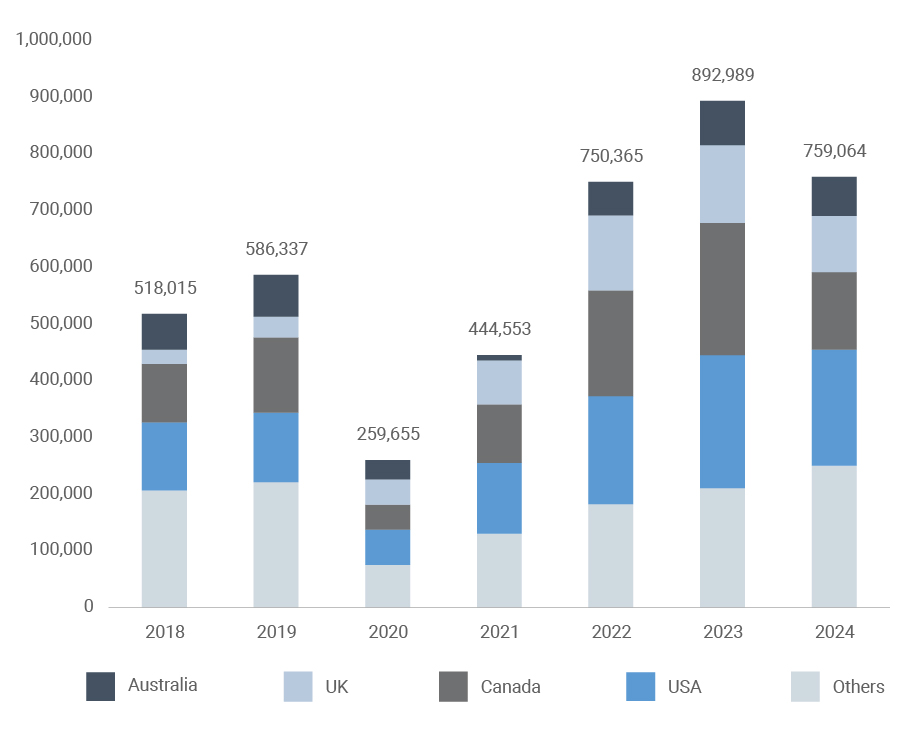

For many Indian students and their families, studying abroad has long been viewed as an investment in a better future. The number of Indian students overseas increased from nearly 518,000 in 2018 to a peak of 893,000 in 2023, according to data from the Indian Ministry of External Affairs. However, this peak was partly driven by pent-up demand following the pandemic. As that demand began to subside in 2024, the number of Indian students studying abroad fell by 15% — or nearly 134,000 students — to 760,000.

With rapid changes to immigration and visa policies in the USA, followed by Canada in 2025 — two of the most popular destinations — the number of Indian students studying abroad is likely to decrease further in the near term. These policy shifts highlight the increasingly complex relationship between global mobility policies and international education pathways.

Chart 1 Number of Indian Students Abroad by Top 4 Countries (2018–2024)

Analysis by Dr. Rahul Choudaha

Source: Indian Ministry of External Affairs

One notable feature of Indian students’ study abroad choices is their concentration in the ‘big four’ English-speaking countries — Australia, Canada, the UK, and the USA. In 2024, two out of three Indian students studying overseas, or around 509,000, were enrolled at tertiary institutions in one of these four countries. Another characteristic is concentration by level and field of study. For example, approximately three in four (77%) Indian students pursue master’s degrees in STEM fields, according to US Department of Homeland Security data.

Overall, these study abroad enrollment patterns, coupled with headwinds in key destination countries, suggest that there is unmet demand among Indian students and their families are willing to invest in global learning.

At a time when student mobility options are tightening and uncertainty about recovering educational investment is rising, the aspirations of students and parents for alternatives are converging with the arrival of foreign universities in India under a new regulatory framework.

Catalyzed by the National Education Policy (NEP) 2020 and related regulations, global universities ranked in the top 500 globally are now permitted to establish IBCs in India. To put this in perspective, only four Indian institutions appear in the top 500 of the Times Higher Education World University Rankings 2026, and nine in the QS World University Rankings 2026 top 500. Currently, at least 18 foreign universities are preparing to launch academic programs in India beginning in August 2026, the majority from Australia and the UK. Given Indian students’ strong preference for the ‘big four’ English-speaking destinations and the unmet demand for global learning, it is likely that a segment of Indian students will enroll at these IBCs.

From the perspective of foreign universities, the change in Indian policy offers an opportunity to engage with students who are facing increasing barriers owing to tightening visa and immigration policies. For the Indian government, the entry of foreign universities represents a new pathway for internationalizing the domestic higher education system, building capacity, enhancing quality, retaining talent, and conserving foreign exchange.

When deciding where to study, students consider a number of factors, such as cost, admissions and visa requirements, career prospects, and personal goals. IBCs represent an emerging option that sits between studying overseas and enrolling at a domestic university.

The total cost of studying at an IBC can be up to half that of studying abroad, largely owing to lower tuition fees and savings on living expenses. At the same time, international campuses are typically two to three times as expensive as domestic private universities, placing them within a middle price range for families seeking internationally oriented programs.

IBCs therefore expand the range of options available to Indian students at both the undergraduate and postgraduate levels. At the undergraduate level, some students who may currently be priced out of overseas study due to higher costs or immigration uncertainties could begin their studies at an IBC and later pursue a master’s degree overseas.

For female students, IBCs may broaden access. For instance, only about one-third of Indian students in the USA are female, often due to parental concerns about safety and cultural differences. International campuses within India may provide an alternative pathway for some of these students.

In the short term, master’s students who are unable to go overseas, or who prefer to avoid uncertainty around post-study job prospects may earn global degrees at IBCs.

International campuses do not replicate or replace the immersive experience associated with studying abroad. Instead, they offer something unique to a growing segment of students who want to pursue global degrees at home. The arrival of international campuses — at a time when Indian student mobility is facing constraints — opens a new set of choices for students seeking global learning. Over time, these developments may reshape how families balance international education aspirations with evolving mobility pathways.

As the global leader in residence and citizenship planning, Henley & Partners is best placed to advise you and your family. Contact us for a free consultation.